U.S. Oil Drilling: Small U.S. shale producers are cutting back on drilling as oil prices drop to multi-year lows and tariffs raise construction costs, threatening future production growth. While U.S. output is still expected to hit a record 13.7 million barrels per day in 2025, both the EIA and IEA have trimmed their forecasts due to the impact of tariffs and weakening demand. Companies like Blackridge Resources and Arena Resources are scaling back or delaying drilling plans, citing uneconomical returns at $60 oil and rising steel costs from tariffs. U.S. crude briefly hit a four year low of before rebounding, but volatility continues amid trade tensions. Oilfield service firms like Baker Hughes and Halliburton are already feeling the revenue pinch from the drilling slowdown, with analysts predicting that shale spending will decline in tandem with falling prices. Despite the downturn, some producers see opportunity, using the lull to acquire acreage and prepare for a market rebound.

OPEC+: Investor concerns have emerged over a potential increase in OPEC+ output, leading to a nearly 2%-3% drop in oil prices. Reports suggest that several OPEC+ members may push for increased production in June, raising fears of oversupply in the market. Tensions within the group persist, as Kazakhstan stated it will prioritize national interests over quota commitments, echoing past disputes that led to Angola's exit from OPEC+. Analysts warn that continued discord may lead to a price war, further destabilizing the market. These developments have contributed to cautious movements in oil prices.

Ukraine-Russia: Russia and Ukraine exchanged fresh accusations over the lack of progress in peace talks, with Moscow blaming Ukrainian President Zelenskyy for obstructing diplomacy, while Kyiv accused Russian President Putin of prolonging the war. U.S. President Donald Trump threatened to withdraw from peace efforts if both sides fail to reach a deal soon and angered Zelenskyy by dismissing Crimea as a non-negotiable issue. Crimea remains a major sticking point, with Zelenskyy refusing to recognize the 2014 Russian annexation, which Russia insists is non-negotiable and historically justified. Russia criticized Zelenskyy for refusing concessions and allegedly derailing a recent round of peace discussions in London. Kyiv condemned a deadly Russian missile and drone strike on the capital as proof of Moscow's disinterest in real peace. Despite international calls for a truce, both sides remain entrenched, with Ukraine demanding a just peace and Russia setting conditions that Kyiv sees as stalling tactics.

Market Overview: The energy sector is starting out bearish this morning sustained by the easing of U.S.-China trade tensions and potential shifts in Federal Reserve policy. WTI is poised for a weekly loss of approximately 2.3%, attributed to concerns over oversupply from OPEC+ and global demand uncertainties. Additional downward pressure stemmed from a stronger U.S. dollar and potential diplomatic developments that could increase global oil supply as well as balancing geopolitical developments with fears of a supply glut. Energy futures making little moves with crude down $0.81 to $61.98, HO is down $0.0067 to $2.1370, and RBOB is down $0.0125 to $2.0932.

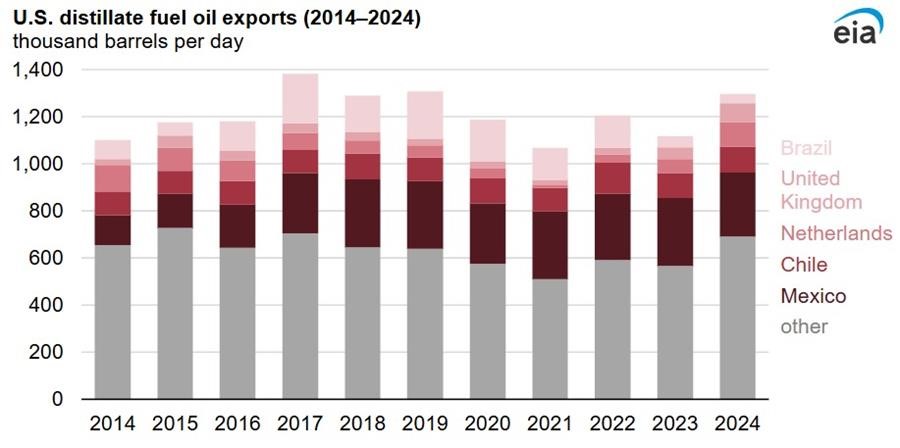

In 2024 Mexico was the largest destination for U.S. distillate exports, receiving 272,000 barrels per day, or 21% of total exports. Other major destinations included Chile, 110,000 barrels per day, the Netherlands, 103,000 barrels per day, the UK 81,000 barrels per day, and Peru 74,000 barrels per day. Brazil, once the second largest importer over the previous decade, reduced its imports to 41,000 barrels per day in 2024 due to increased purchases of discounted Russian distillate following European sanctions on Russia. This shift contributed to a rise in U.S. distillate exports to European hubs like the Netherlands and the UK, which significantly increased their imports from 2021 levels. U.S. motor gasoline exports in 2024 totaled 877,000 barrels per day, a decrease of 24,000 barrels per day from 2023. Mexico remained the top destination for U.S. gasoline, accounting for 495,000 barrels per day, with other major importers located primarily in the Western Hemisphere.

The energy complex saw markets bearish to start out the day then gain momentum mid morning to end the day bullish. Global oil prices have remained relatively stable this week even with a perplexing DOE report regarding supply and demand positions. OPEC+ continues to signal production discipline, while geopolitical tensions in the Middle East add a risk to crude oil prices. A meeting between President Vladimir Putin and President Trump occurred today which had a very constructive stance to end the war in Ukraine hopefully soon, which if the war ended it could add more supply to global markets. To end the week crude oil finished bullish by $0.23 to $63.02 a barrel, HO up to $2.1673, and RBOB up to $2.1189.