UAE: The UAE has signaled it could boost its oil capacity beyond 5 million barrels per day after 2027, potentially reaching 6 million bpd if market demand justifies it, according to Energy Minister Suhail al-Mazrouei. While 6 million bpd is not an official target, achieving it would make the UAE the fourth-largest oil producer globally, behind the U.S., Saudi Arabia, and Russia. OPEC+ granted the UAE a higher production quota this year, following its significant investment in expanding capacity from 3 million to 4.85 million bpd. Capacity debates have caused tensions within OPEC+, including Angola's 2024 exit and disputes over overproduction by Iraq and Kazakhstan, which have frustrated Saudi Arabia. In response, OPEC+ tasked specialists in May with developing a system to assess members’ true capacity for setting 2027 quotas. Despite near-term demand concerns, the group is currently raising production and expects to increase output by 2.5 million bpd between April and September 2025, while 3.65 million bpd in cuts remain in place until the end of 2026.

SPR: A recently signed U.S. budget bill significantly reduced funding for refilling the Strategic Petroleum Reserve (SPR), despite earlier statements supporting a full replenishment. The SPR, the world's largest emergency oil storage, can hold up to 714 million barrels but contained only 403 million barrels as of July 4, well below its 2010 peak of 727 million. Reserve levels dropped to a40-year low in 2023 following major releases aimed at stabilizing oil prices during global supply disruptions. Fully refilling the SPR would cost over $21 billion at current crude prices and require several years. The new bill decreased funding from $1.3 billion to $171 million for repurchases between 2025 and 2029, prompting debate over whether maintaining such a large reserve is still necessary given recent changes in the U.S. energy sector.

IEA: The International Energy Agency (IEA) reports that the global oil market may be tighter than it seems, despite forecasts showing a surplus due to higher supply than demand. While global oil supply is expected to rise by 2.1 million barrels per day (bpd) in 2025, demand is projected to grow by only 700,000 bpd—its slowest pace since 2009, excluding the pandemic year. However, strong seasonal demand for travel and power generation in the Northern Hemisphere is pushing refineries to boost processing, absorbing much of the supply and tightening the market. Price indicators such as strong refining margins and steep backwardation suggest physical tightness, despite the apparent surplus. OPEC+'s recent decision to increase output had little market impact, with oil prices still rising, indicating strong demand. The IEA also noted that U.S. tariffs might be affecting demand in countries like China, Japan, and Mexico, and its forecasts remain more conservative than OPEC's due to expectations of a faster energy transition.

Market Overview: Oil prices rose by about 1% on Friday, with U.S. West Texas Intermediate (WTI) crude climbing to $67.39 a barrel, as investors balanced signs of near-term market tightness against forecasts of a surplus later this year. The International Energy Agency (IEA) said summer refinery demand is supporting prices, even though supply is expected to outpace demand over the year. Analysts noted that despite OPEC+ plans to boost output, short-term demand remains strong, especially with high August shipments of Saudi crude to China. Geopolitical tensions also contributed to market uncertainty, as investors watched for potential new U.S. sanctions on Russia and a proposed EU price cap on Russian oil. Meanwhile, longer-term demand forecasts were trimmed by OPEC, citing weaker growth expectations from China.

OPEC launched its latest oil outlook report at a biennial seminar in Vienna, though it barred access to reporters from Reuters and other media outlets without explanation. The report states that global oil demand has fully recovered from the COVID-19 pandemic, creating a more predictable outlook. However, demand growth in China is slowing due to weaker economic conditions, increased EV adoption, and oil substitution. Since April, OPEC+ has gradually increased output, but separate production cuts of 3.65 million barrels per day remain in effect until the end of 2026, with no current plans to release that oil. OPEC maintains its 2030 demand forecast at 113.3 million bpd, significantly higher than the IEA’s projection of a peak at 105.6 million bpd by 2029. Looking long-term, OPEC expects growth to come from India, Africa, and the Middle East, citing slower energy transitions in developing countries. It now forecasts global oil demand to reach 122.9 million bpd by 2050 and estimates the oil sector will need $18.2 trillion in investment through that year.

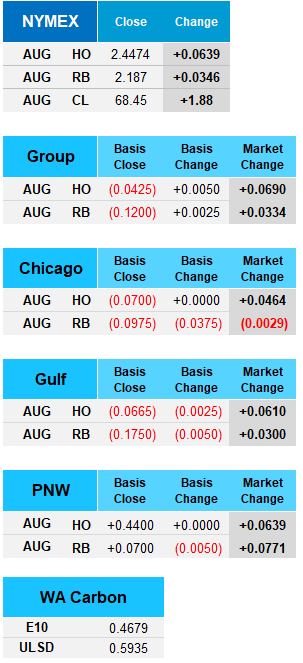

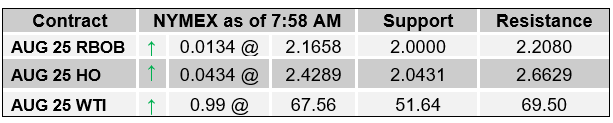

U.S. West Texas Intermediate (WTI) crude rose 2.8% on Friday to $68.45 a barrel, marking a weekly gain of about 2.2%, as the International Energy Agency (IEA) said the oil market is tighter than it appears due to strong summer refinery demand. Despite this short-term tightness, the IEA also forecast a supply surplus later in the year, as it raised its supply growth outlook and trimmed demand projections. U.S. drillers cut oil and gas rigs for the 11th straight week, further signaling tightening demand, while Saudi Arabia is expected to ship a two-year high of 51 million barrels to China in August. Geopolitical concerns also added to market volatility, with potential new U.S. sanctions on Russia and a floating EU oil price cap under discussion. Meanwhile, OPEC reduced its long-term demand outlook due to weaker Chinese consumption growth, even as short-term prices remain supported by travel-related fuel demand and limited production increases.