U.S.-European Union (EU) trade deal: Over the weekend, in Scotland, European Commission President Ursula von der Leyen and U.S. President Donald Trump announced a framework trade agreement had been struck. The U.S., after months of negotiations, will be imposing a 15% import tariff on most EU goods (which is half the threatened rate). In addition, the EU plans to significantly increase purchases of U.S. military equipment and energy with a$600 billion investment in the United States. These two allies account for around a third of global trade. This deal is indicated to be similar to last week’s $550 billion agreement with Japan. German Chancellor Friedrich Merz was also positive about the deal which he indicated would avert a trade conflict that would have negatively affected Germany’s export-driven economy along with its large auto sector. There is some scrutiny as to how the EU will be able to achieve such lofty increases in purchasing of U.S. energy but President Trump does still retain the ability of increasing tariffs in the future if EU does not live up to investment commitments.

OPEC+: The Joint Ministerial Monitoring Committee (JMMC) is a panel of top ministers from the Organization of the Petroleum Exporting Countries and allies led by Russia (OPEC+). These folks meet about every two months and will be having one of those discussions today as their role is to monitor conformity with production adjustments while reviewing overall market conditions. They do have potential to call for a full meeting of OPEC+ to address market developments if deemed necessary. OPEC+ represents about half of the world’s oil production and is slated to have separate meeting on August 3rd with anticipation they will agree to further 548,000 barrel per day (bpd) increase for September aftermost recent decision indicated 548,000 bpd increase in August. Despite the increases (which is basically an unwind of 2.2 million bpd production cut), prices have seen support considering summer demand as well as some of members not increasing production as much as quota hikes would suggest.

U.S.-China trade: After the June preliminary deal on tariffs, China is now currently facing an August 12th deadline to reach a durable tariff agreement with the U.S. A meeting, which would be third round of talks, is set for today in Stockholm between senior Chinese and U.S. negotiators to address the economic disputes in the trade war between the world’s top two economies. Broader economic issues will eventually come into play as the U.S. has complaints that China’s export-driven model is overwhelming world markets with cheap goods while China has concerns that the U.S. national security export controls on tech goods seeks to impede Chinese growth. Analysts suggest U.S.-China negotiations will require additional time considering they are far more complex with China’s control on global markets for rare earth minerals and magnets posing a significant challenge for U.S. industries. The expectation from today’s activity is for there to be a 90-day extension regarding the tariff and export control truce which is in place that would possibly set the stage for a late October meeting between China’s President Xi Jinping and Trump.

Market Overview: Considering the EU/US trade deal struck over the weekend, energy is beginning the week on a positive note as both crude and products are showing solid advancement. This deal removes another layer of uncertainty and allows focus to shift back to fundamentals. West Texas Intermediate (WTI) crude has found support at $65 level but there are struggles finding interest above $69 considering OPEC+ supply increase is on the horizon.

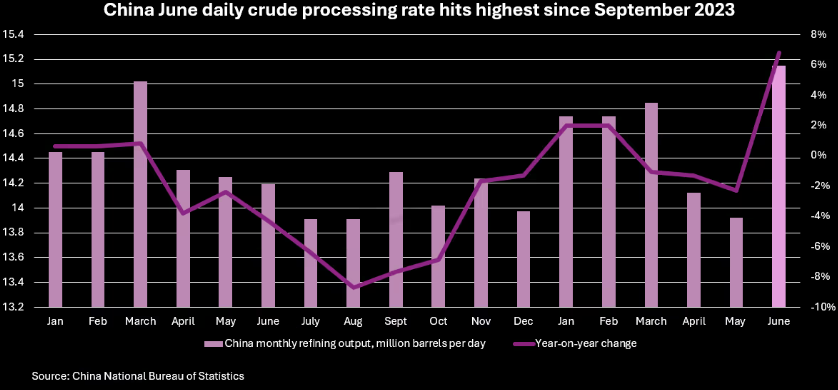

China's refiners increase crude processing

China’s state-owned refiners had a heavy maintenance period during April and May before June saw a very strong output as the country’s overall refining throughput for the month was at 15.15 million bpd. This marked the highest such level since September 2023 and was much needed after product stocks had gotten quite low. Per Ye Lin, a vice president with Rystad Energy, “demand for jet fuel and petrochemical feedstocks is growing healthily in China, driving more supply from the state-owned refineries.” In addition to the oil demand growth (estimated by Barclay’s to be about 330,000 bpd year-on-year during the first half of 2025), gasoline and diesel stocks are at six-year lows in July. These increases in crude processing rates are anticipated to last through the third quarter which should drive up imports by the world’s largest oil importer.

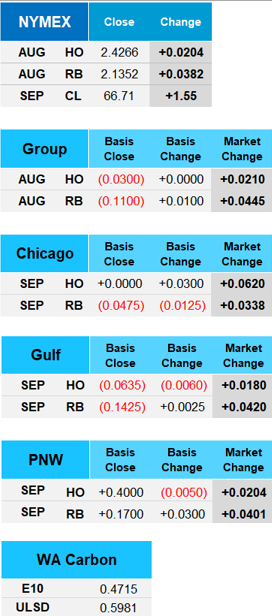

The weekend's trade deal struck between the U.S. and the European Union (EU) provided support to the market as West Texas Intermediate (WTI) crude gained +$1.55 (to $66.71) on the day. A more than 2.37% advancement during the session. The products did not show as significant of an increase on the day but did move higher as well with RBOB gasoline moving +$0.0382 (to $2.1352) and ULSD distillates showing smallest move during the day as was up $0.0204 (to $2.4266) but did break a streak of four consecutive settles in the red. President Trump also expressed frustration with Russian President Putin and suggested massive secondary sanctions if Russia was unable to find a truce with Ukraine. WTI crude values even briefly moved above $67 on that particular news this morning.