Russia: U.S. President Trump has become quite frustrated with Russian President Vladimir Putin and his lack of progress towards ending 3 ½ year-old conflict with Ukraine. Earlier this month, Mr. Trump had initiated a 50-day deadline to see some action or face consequences but yesterday that timeline was shortened to 10 or 12 days as he indicated “there’s no reason in waiting… we just don’t see any progress being made.” Despite previous hesitancy to do so, the newly indicated deadline suggests he is ready to move forward on threats to sanction both Russia as well as buyers of its exports. There was no immediate feedback from the Kremlin. These potential sanctions do raise oil supply concerns.

The Fed: The U.S. central bank (or the Fed) has a meeting this week and is scheduled to release the Fed’s policy statement tomorrow (Wednesday, July 30th). There has been some mixed economic sentiment recently as housing and construction has shown a bit of weakness while consumer spending is strong. Vigorous debate about whether to leave interest rates unchanged is anticipated amongst the Federal Reserve governors as President Trump has been strongly advocating to lower them in recent months. The majority of Fed policymakers are concerned about tariffs (like 15% recently set for European Union as well as Japan) and what could mean to the progress being seen in bringing inflation to central bank’s 2% goal. The expectation is for rates to remain in 4.25%-4.50% range.

U.S. trucking activity: The American Trucking Association (ATA) indicated that June showed a second consecutive month of declines in trucking activity as the trade group’s seasonally adjusted For-Hire Truck Tonnage Index was at 113.3 after being at 113.8 in May. For the entire 2nd quarter activity was basically flat as was up 0.2% from first quarter but down 0.2% from same period one year prior. The ATA index is quite strong in contract freight compared to traditional spot market freight and the tonnage index is based on surveys of its 37,000 members. Trucking is considered a barometer of U.S. economic activity as the industry comprises 72.7% of tonnage carried by U.S. freight transportation.

Market Overview: The Complex is beginning the day mixed as crude is gaining some support considering potential further sanctions on Russia while the products show ulsd distillates slightly lower to begin the session and rbob gasoline is moving higher and is above the $2.15 level. The American Petroleum Institute (API) will release weekly inventory data later this afternoon.

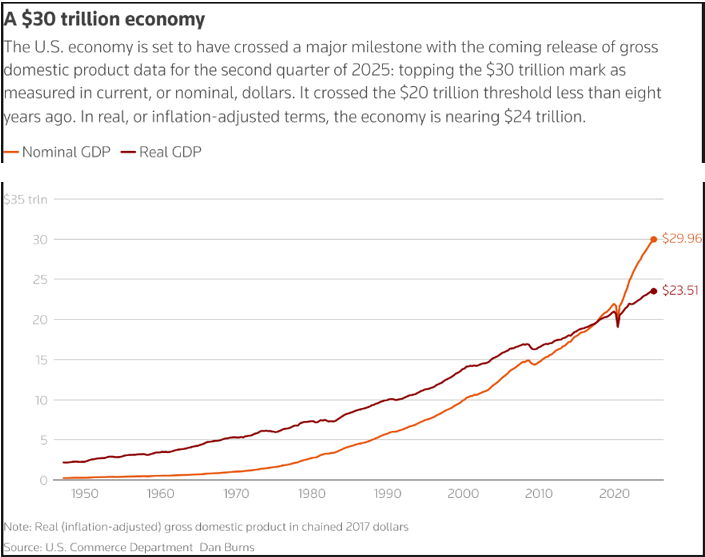

U.S. economy milestone

As Fed decision looms on interest rates, the Commerce Department will be reporting on second quarter economic activity. The anticipation is for this to show are acceleration during this period with total output, for the first time, being above $30 trillion in non-inflation-adjusted terms. As you can see on chart above, this nominal Gross Domestic Product (GDP) crossed $20 trillion less than 8 years ago. Consumer spending is about two-thirds of economic output and has shown recent strength with June’s retail sales a particular positive as they were up more than anticipated.

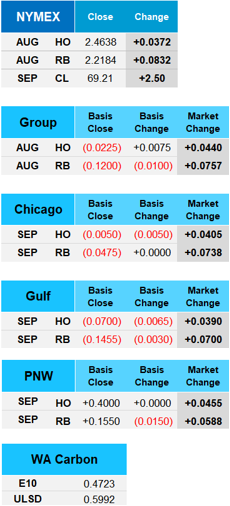

Today's session began mixed before moving decidedly to higher ground for both products and crude. The gradual increase on day was the market reacting to optimism that a trade war between U.S. and major trading partners was subsiding, plus, President Trump is providing additional pressure for Russia to end fighting with Ukraine. West Texas Intermediate (WTI) crude got near $70 during the day's activity before advancing $2.50 (to $69.21) at the settle. RBOB gasoline moved +$0.0832 (to $2.2184) while ULSD distillates showed smallest move during the day but was still up $0.0372 (to $2.4638). The American Petroleum Institute (API) will also be providing its weekly supply updates yet this afternoon.