U.S. economy: Today’s advance estimate of second-quarter Gross Domestic Product (GDP) by the Commerce Department’s Bureau of Economic Analysis showed are bound more than anticipated. GDP increased by a 3.0% annualized rate during the quarter (when 2.4% was expectation) after contracting at 0.5% pace during the first quarter of 2025. Economists are indicating the main GDP figure is quite distorted by trade considering the heavy focus on tariffs during first half of the year as inventories and trade are most volatile components of GDP. Second quarter inflation was also reported to be 2.1% after anticipation of it to be 2.9%. Economists are anticipating lackluster economic growth during second half of the year.

Russian oil: The largest buyer of Russian oil is China at about 2 million barrels per day (bpd). Earlier this week, U.S. President Trump shortened the deadline for Russia to make progress towards a peace deal with Ukraine or its oil customers would be assessed secondary tariffs of 100% in 10 to 12 days. Two days of U.S.-China trade talks wrapped up yesterday in Stockholm and U.S. Treasury Secretary Scott Bessent used those discussions to warn Chinese officials that continued purchases of sanctioned Russian oil would result in the sizable tariffs considering legislation in U.S. Congress that authorizes Trump to levy tariffs up to 500% on countries that purchase sanctioned Russian oil. China countered with suggestion they would protect its energy sovereignty. Bessent added, “so I think anyone who buys sanctioned Russian oil should be ready for this.” India and Turkey are the next largest purchasers. JP Morgan analysts suggest India will comply with the U.S. sanctions while China is unlikely to do so.

U.S. weekly inventory: The Energy Information Administration (EIA) will provide its weekly data this morning with expectation that there will be draws across the board. Yesterday’s industry update from the American Petroleum Institute (API) showed a bit of a bearish look, however, as crude inventory actually showed a 1.54 million barrel build and distillates had an even larger increase of 4.19 million barrels. Gasoline stocks did drawdown by 1.74 million barrels which is slightly more than anticipated.

Market Overview: The market is weighing supply risks with mixed start early in the session as crude is advancing slightly and products are flat to weaker. RBOB gasoline had a particularly strong day yesterday (as was up more than $0.08 on the day) with highest settle since June 21st. Today’s attention will focus on the Fed meeting (and whether there is any change to interest rates) as well as this morning’s weekly EIA inventory data.

European diesel and jet fuel imports

As harsher U.S. sanctions regarding Russian oil appear on the cusp, Europe has already experienced quite a shift away from importing Russian diesel and jet fuel in recent years. In 2021, 40% of Europe’s diesel imports came from Russia but when 2022 war broke out they instead increased imports from China, India, and Turkey. Yet, those 3 countries had also greatly increased imports of cheap Russian crude oil. Thus, they were effectively getting products made from the Russian feedstock. Recently, the European Union (EU) also adopted its 18th package of sanctions against Russia over fighting with Ukraine as attempt to limit revenue from its oil exports. This includes an import ban on refined products made from Russian crude and that is likely to begin next year.

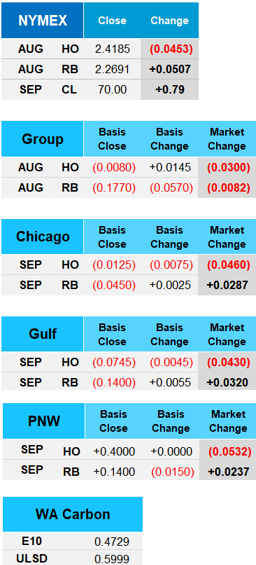

Despite today's weekly Energy Information Administration (EIA) report showing an unexpected significant build (of 7.7 million barrels) for crude inventory, West Texas Intermediate (WTI) crude was able to move higher and even had first settle above $70 since June 20th. Also, a narrowing spread between WTI and Brent crude resulted in a significant decline in U.S. crude exports during the period (as they fell by 1.2 million bpd compared to previous week). The products were mixed as RBOB gasoline advanced for third consecutive session and was up $0.0507 (to $2.2691) while ULSD distillates were off $0.0453 (to $2.4185). The Fed also reiterated focus on controlling inflation with decision to hold interest rates at U.S. central bank steady in 4.25% to 4.50% range. This decision came after a 9-2 vote by Federal Open Market Committee and the two Fed governors dissenting on the vote represented the first time that had occurred in more than 30 years. The Fed's next meeting is slated for September 16th-17th.