India: With President Trump threatening 100% tariffs on countries that buy Russian oil, it appears that Indian state refiners have halted doing so in the past week. India is the world’s third-largest oil importer and has been main buyer of seaborne Russian crude. Four state refiners (Indian Oil Corp, Hindustan Petroleum Corp, Bharat Petroleum Corp, and Mangalore Refinery Petrochemical Ltd) have been regularly buying Russian oil on a delivered basis but instead have turned to spot markets for replacement supply that is mostly comprised of Middle Eastern grades.

U.S. gasoline demand: Yesterday’s weekly Energy Information Administration (EIA) data showed a considerable increase on crude inventory when a draw was anticipated as stockpiles were up 7.7 million barrels last week. However, gasoline demand in the country was quite strong as product supplied showed it was at 9.2 million barrels per day (bpd) compared to just under 9 million bpd the previous week. This resulted in a larger than anticipated decline in stocks as they fell by 2.7 million barrels when less than a 1 million barrel draw was the expectation. The front month (AUG25) RBOB gasoline contract has seen a pretty strong move higher this week as well as has advanced more than 8% in the first few days. Distillates showed a 3.6 million barrel build when a 300,000 barrel increase was the expectation.

Iran: In an effort to make Iranian oil sales more difficult, the U.S. Treasury Department announced a fresh round of sanctions yesterday that are the most significant since 2018. As a further action of “maximum pressure” campaign, these sanctions were imposed on over 115 Iran-linked individuals, entities, and vessels with a broad target on shipping interests of Mohammed Hossein Shamkhani who is the son of Ali Shamkhani, an adviser to Supreme Leader Ayatollah Ali Khamenei. A senior White House official indicated last week that the U.S. is open to again talking directly with Iran after there was five rounds of talks between the two nations before the airstrikes occurred in June. Considering those actions, both European and Iranian diplomats have indicated there is little prospect of Iran coming to the negotiating table at this time.

Market Overview: As the month of July wraps up that means the AUG25 contracts for both ULSD and RBOB will also be expiring after today and rolling to next month. Crude and products are both showing small losses early and distillates continue to trade sideways in a relatively narrow range of $2.38 to $2.48. For WTI crude, yesterday saw it move above $70 but has already fallen below that this morning so will be of note if can maintain that level in coming days. With Fed’s decision behind us that they will be keeping interest rates steady for now the market will next look to the OPEC+ meeting over the weekend and how they suggest they’ll be moving forward on crude production.

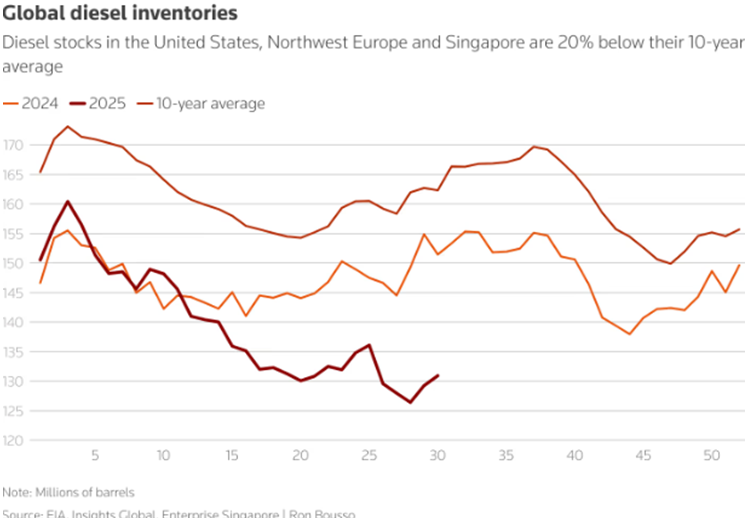

The diesel market is seen as an indicator of overall global economic activity considering its use in ships, trucks, and power generators along with industrial and agricultural machinery. Plus, in Europe, around a quarter of passenger cars run on it which is significantly greater than other regions. In 2025, usage was anticipated to be weak as President Trump took office and initiated global trade war. Yet, demand has proven to be quite resilient. India and China are both showing recent signs of strong demand for the fuel while U.S. four-week average is indicating to be nearly 5% higher than one year ago. As can be seen in chart above, current global diesel inventories are off considerably compared to 2024 and even more so compared to 10-year average. The resilient demand along with unplanned outages/closures of refineries in England and Israel are significant contributors to low global inventory. Plus, a global shortage of heavy and medium crude grades (that provide higher diesel yields) is also impacting the result of lower refinery output.

Both crude and products experienced losses during final session of July as AUG25 contracts expire for both RBOB and ULSD. Tariffs are causing some concern regarding demand and OPEC+ will meet on Sunday with expectation of further production increases which is resulting in some market pressure. On the day, RBOB gasoline fell $0.0535 (to $2.2156) while ULSD distillates were off $0.0190 (to $2.3995) and WTI crude was not able to maintain above $70 level as ended at $69.26 (a decline of $0.74). Even though today was weaker the entire month showed positivity as RBOB gasoline had biggest gain (of over 6.5%) while WTI crude was close behind (@ +6.37%) and ULSD distillates advanced 2.29%.