U.S. Oil: The U.S. Energy Information Administration (EIA) has lowered its 2025 oil production forecast to 13.37 million barrels per day (bpd), down slightly from the previous estimate of 13.42 million bpd, due to falling oil prices and reduced drilling activity. Despite this revision, production would still mark a record high and remain steady into 2026. The downgrade reflects challenges from economic uncertainty caused by President Trump’s fluctuating tariff policies ,rising OPEC+ output, and geopolitical tensions involving Iran and Israel. The EIA also raised its price forecasts for both Brent and West Texas Intermediate (WTI) crude due to geopolitical risks, though it expects global inventory growth to put downward pressure on prices over time. U.S. oil demand is projected to rise modestly to 20.4 million bpd in 2025 and remain steady in 2026.

API: The American Petroleum Institute (API) estimated a surprise crude oil inventory build of 7.130 million barrels, sharply contrasting with market expectations. It also reported a distillate fuel draw of 830,000 barrels and a gasoline draw of 2.180 million barrels, suggesting strong fuel demand despite the crude build. In contrast, a Reuters poll of analysts had forecast a crude draw of 2.071 million barrels, a distillate draw of 314,000 barrels, and a gasoline draw of 1.486 million barrels. The large divergence between the API's reported crude build and the Reuters consensus draw highlights ongoing uncertainty in supply and demand dynamics.

EIA Price Forecast: The Energy Information Administration (EIA) raised its oil and fuel price forecasts for the second half of 2025 due to heightened geopolitical tensions following the Israel-Iran conflict. However, it lowered its 2026 outlook based on expected global oil inventory builds, while noting its current forecasts were made before OPEC+ announced a larger-than-expected 550,000 bpd output hike starting in August. EIA now expects West Texas Intermediate (WTI) crude to average $64.69 per barrel in Q3 and $60.02 in Q4, with full-year 2025 prices averaging $65.22; 2026 prices are forecast to decline to $54.82. Wholesale diesel prices are also projected to rise in Q3 and Q4 due to low U.S. inventories, with retail diesel prices expected to reach $3.67/gal in Q3 and $3.59/gal in Q4. Gasoline price forecasts saw only slight adjustments, with Q3 retail prices cut slightly to $3.11/gal and Q4 raised to $2.99/gal. U.S. oil production is forecast to dip slightly in Q3 before rebounding in Q4, averaging 13.37 million bpd this year and in 2026, while U.S. and global petroleum consumption forecasts remain unchanged.

Market Overview: Oil prices remained steady on Wednesday, driven by renewed Red Sea attacks and expectations of lower U.S. oil production in 2025. The attacks, attributed to Yemen's Iran-backed Houthi militia, included a deadly strike that sank a cargo ship, raising geopolitical tensions. The U.S. Energy Information Administration forecasted reduced oil output next year due to falling prices, which supported the price rally. Meanwhile, uncertainty surrounding U.S. tariffs under President Trump and a possible 7.1 million barrel crude inventory build added mixed pressures to the market. Despite planned OPEC+ supply increases, analysts note that the market continues to absorb the extra barrels, signaling strong demand.

The candlestick chart shows a recent rebound in WTI crude oil prices, supported by the RSI rising to 55.75—signaling a shift from bearish to more neutral-to-bullish momentum. This recovery aligns with a larger-than-expected drawdown in U.S. crude inventories reported by the EIA, pointing to tighter supply, alongside geopolitical tensions that have added a risk premium to prices. Despite this upward move, gains remain modest as concerns over weak Chinese demand continue to pressure the global outlook. Additionally, uncertainty around future U.S. interest rate cuts is dampening investor sentiment. As a result, further upside in the crude market remains limited for now.

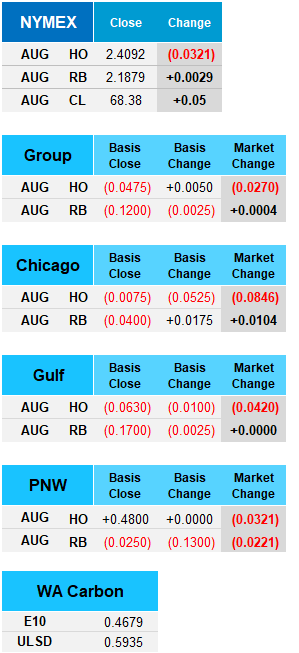

Oil prices were steady on Wednesday, with U.S. West Texas Intermediate (WTI) crude closing up 5 cents at $68.38 a barrel, as markets balanced strong U.S. gasoline demand, rising crude inventories, and renewed attacks on Red Sea shipping. U.S. crude stockpiles unexpectedly rose by 7.1 million barrels, while gasoline demand jumped 6% to 9.2 million barrels per day, indicating resilient consumer activity. The Houthi militia claimed responsibility for sinking two ships in the Red Sea, reigniting geopolitical concerns in a vital shipping lane. Meanwhile, the EIA forecast lowered U.S. oil production in 2025 due to declining prices and reduced drilling activity. President Trump announced a 50% tariff on copper to support domestic production, creating trade uncertainty despite delaying implementation until August 1. OPEC+ plans to boost oil output again in September, but analysts say the market is absorbing the added supply without increasing inventories, suggesting continued strong demand.