OPEC+ gears up for large August output increase: OPEC+ is preparing to ramp up production by another 411,000 barrels per day (bpd) in August, bringing the total 2025 supply increase to approximately 1.78 million bpd. This marks a shift from previous deep cuts as the group seeks to regain market share, especially ahead of their July 6 meeting. Increased output, including a 300,000 bpd boost from the UAE, puts downward pressure on WTI prices. Internal divisions persist as members debate compliance and timing. Markets are now weighing the supply surge against demand resilience, setting a cap on wild swings.

California regulator warns fuel margins will rise: California’s Energy Commission is urging state officials to boost fuel imports and temporarily lift its cap on refinery profit margins ahead of two refinery closures. With pipeline disruptions looming, gasoline prices in the state could spike by 15 to 30 cents per gallon, exacerbating already the highest U.S. pump costs (currently about $4.61/gal vs. $3.21 national average). The CEC is advocating for support to keep local refineries operational and expand import terminal capacity. Recommendations also include pausing margin cap policy for additional policy analysis. These developments heighten downstream cost pressures that ultimately feed back into WTI-linked gasoline benchmarks.

War premium drains as ceasefire takes hold: Oil prices are set to record their sharpest weekly decline in nearly two years as the war premium fades on the back of a ceasefire between Israel and Iran. WTI has retreated to around $65.64, retreating from recent highs above $80 seen mid‑June. Analysts attribute the drop to the realization that oil flows remain unthreatened, while U.S. stock draws and interest‑rate speculation offer only limited support. Macquarie forecasts an average WTI of $67 for 2025, citing persistent global oversupply. The combination highlights a market rebalancing with geopolitical fears.

Market Overview: West Texas Intermediate is modestly lower today as markets weigh multiple cross‑currents. The Israel‑Iran ceasefire has sharply reduced geopolitical risk, causing WTI to drop from recent high‑$80 levels. At the same time, U.S. crude stock draws and strong summer gasoline demand (with pump prices notably high in California) provide underlying support. However, looming OPEC+ output increases in August—expected at roughly 411,000 bpd—are capping any significant rally. Downstream, California’s refinery closures and potential margin adjustments threaten to increase gasoline costs locally, feeding demand for imported crude. Traders are now focused on whether OPEC+ formalizes its August hike and how U.S. inventory trends continue through the summer driving season.

Understanding a Candlestick Chart

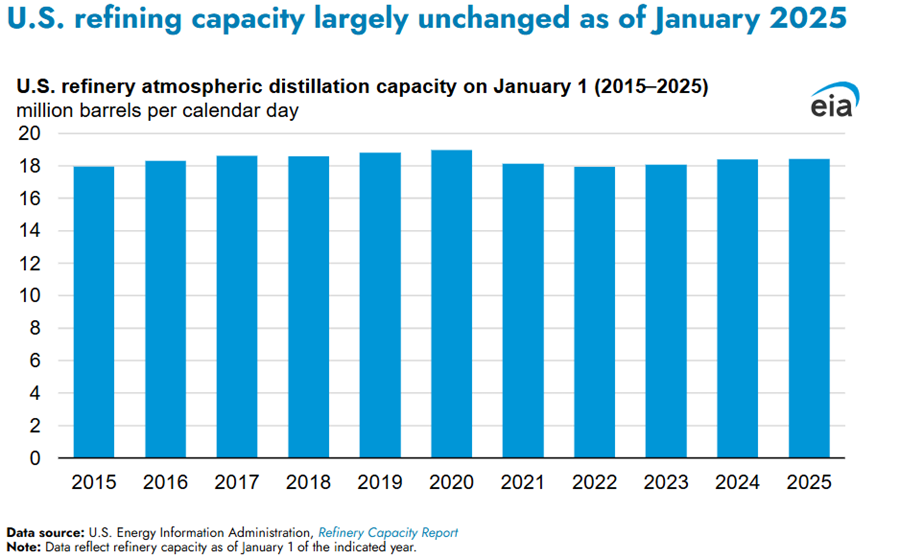

As of January 1, 2025, U.S. operable atmospheric distillation capacity remained steady at 18.4 million barrels per calendar day, showing no significant year-over-year growth. Refinery capacity is measured both by calendar day (accounting for maintenance and downtime) and stream day (maximum output under ideal conditions), with stream day capacity typically about 6% higher. The top three U.S. refiners—Marathon, Valero, and ExxonMobil—reported capacity increases of less than 1%, attributed to minor operational improvements rather than large expansions. No major refinery projects or ownership changes occurred during 2024, contrasting with 2023's notable activity. Motiva’s Port Arthur refinery reclaimed the top spot for calendar day throughput, while Marathon’s Galveston Bay refinery retained its lead in stream day capacity at 665,000 barrels.

Oil prices fell on Monday due to easing tensions in the Middle East and expectations of an OPEC+ production increase in August. WTI dropped, despite being on track for a second monthly gain. A ceasefire following a brief conflict between Israel and Iran reduced supply fears that had pushed prices above $80 earlier in June. U.S. crude production reached a record 13.47 million barrels per day in April, adding downward pressure on prices. OPEC+ is expected to raise output by 411,000 bpd in August, but analysts warn that rising supply could make the market more vulnerable to price weakness.